The June 2022 market insights report is available here Bitcoin.com Exchange. This report and the subsequent ones will provide a recap of crypto market performance and market structure analysis.

Crypto Performance of the Market

The downtrend in crypto markets continues as BTC (and ETH) fell 30% and 44%, respectively, over the past 30 days.

Risk assets continue to face a negative macroeconomic outlook due to high inflation and the tight U.S. labor markets. Crypto has also been hit by a credit crisis, as large crypto-lenders such as Celsius and 3AC have declared bankruptcy.

Despite large losses on BTC/ETH, several high-cap assets are holding strong. Helium, which gained 33% in the past 30 days, was the most positive of all the 50 top market-cap assets. LEO went up by 11.20%, while LINK remained virtually unchanged. AVAX was the worst performer, with Bitcoin Cash down 39%, Cronos (44%), and AVAX (down 44%).

Macro Recap: Commodities pressure despite central bank actions

The U.S. Federal Reserve raised rates by 75 basis point at its latest FOMC meeting. This was the first increase in rates since 1994. The increase was due to continued high CPI data which reached 8.1% in May 2022, the highest level since 1981. The labor market in America remains tight. April data, released on June 1, showed that job openings fell to just 11.4M. This is after a record-breaking March of 11.8M. Chairman Powel hinted at another rate hike of between 50 to 75 bps, which would be announced in the FOMC’s July 2022 meeting.

Supply chain problems and political instability are driving commodities prices up as central banks tighten. The oil market led the charge, with light oils futures hitting $120 USD/barrel before stabilizing over $105 at the end of the last trading session. Higher demand is continuing to be the result of a balance in supply/demand. Even though there was some destruction of demand from higher oil prices, tight supply has been maintained by the supply chain restrictions imposed on Russian exports.

Market Structure: A sign of a local bottom?

BTC markets have seen two forced sell offs of significant size in a month’s time span. Luna Foundation sold assets totaling 80,000 BTC and a large amount of ETH, in order to liquidate their assets. The credit crisis, which saw Celsius, 3AC and Babel Finance liquidated, was second. From November 2021’s all-time peak, the crypto market capitalization declined by $2.1T.

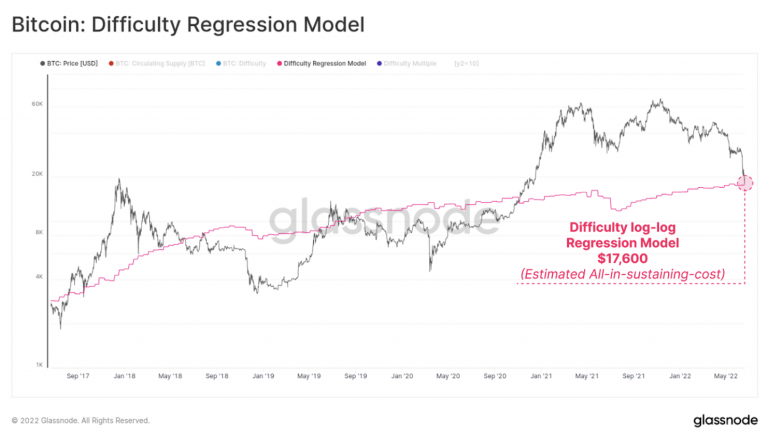

The result is that miners have been under increasing pressure, as they are facing higher electricity bills. The decline in prices means that profitability of miners is declining. According to Glassnode’s difficulty regression model, the “all-in sustaining cost” of mining currently sits at $17,800, which is approximately where BTC traded last weekend.

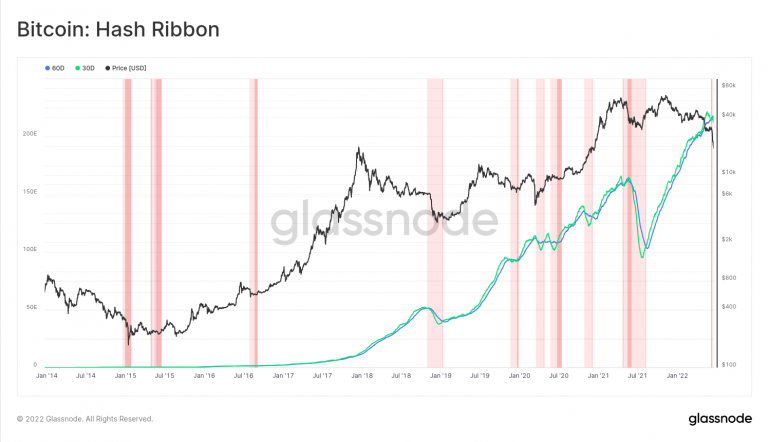

With Bitcoin’s hashrate already down 10% from its all-time-high, it seems unprofitable miners are already going offline.

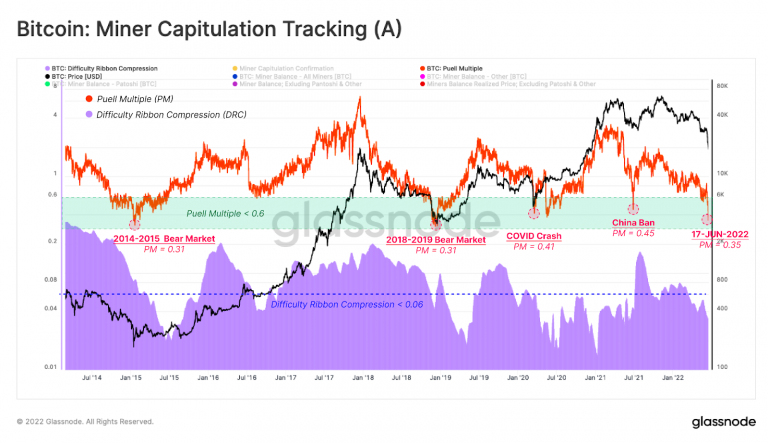

It is possible to argue that miners will be forced sellers as profitability falls. A chart showing the Puell Multiple, (PM), in orange is an oscillator that measures the miners’ revenue. This value is 61% lower than the average yearly revenue. It is similar to levels in 2014/2015, 2018/2019 bear market. Miners experienced a PM multiplier of 0.31 at that point, which was 69% less than the annual average.

The Difficulty Ribbon Compression (DRC), shown in purple in the above chart, is a miner’s stress model. This indicates that mining rigs are offline. It can happen for many reasons. These reasons include regulatory issues, difficulty with the Bitcoin algorithm’s implementation, higher electricity prices, and decreased profitability as a result of low market prices. This chart shows that there has been a drop in the metric. It indicates that fewer active rigs resulted from one of the mentioned reasons.

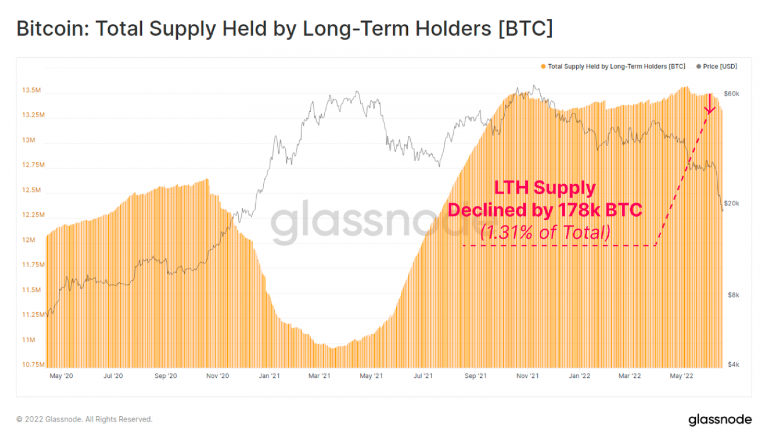

We will next look at Long Time Holders (LTH). LTHs are under pressure as market participants become more cautious. The LTH cohort, with a total supply of 178K BTC, has experienced a decrease in its holdings over the past month. This accounts for 1.31%.

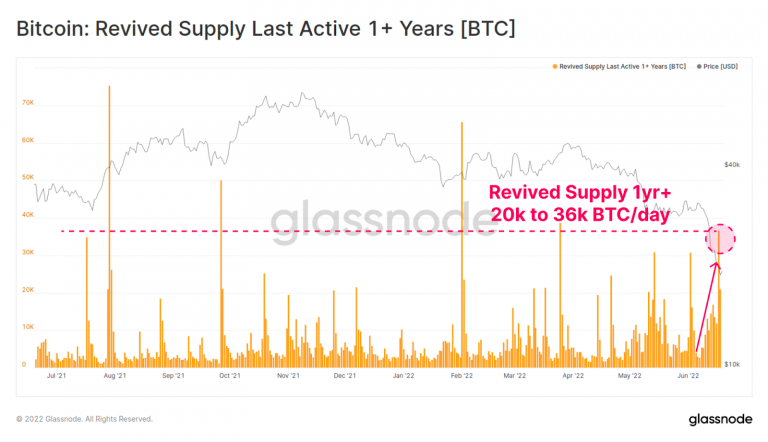

The old supply is another interesting way to assess the state of the sell-off. Below you can see that around 20 to 36K BTC per day are being revived, which is the same as levels in April 22. The fear indicator is interpreted as an indicator of the urgency for long-term holders, which indicates the need to liquidate their position due to current market conditions.

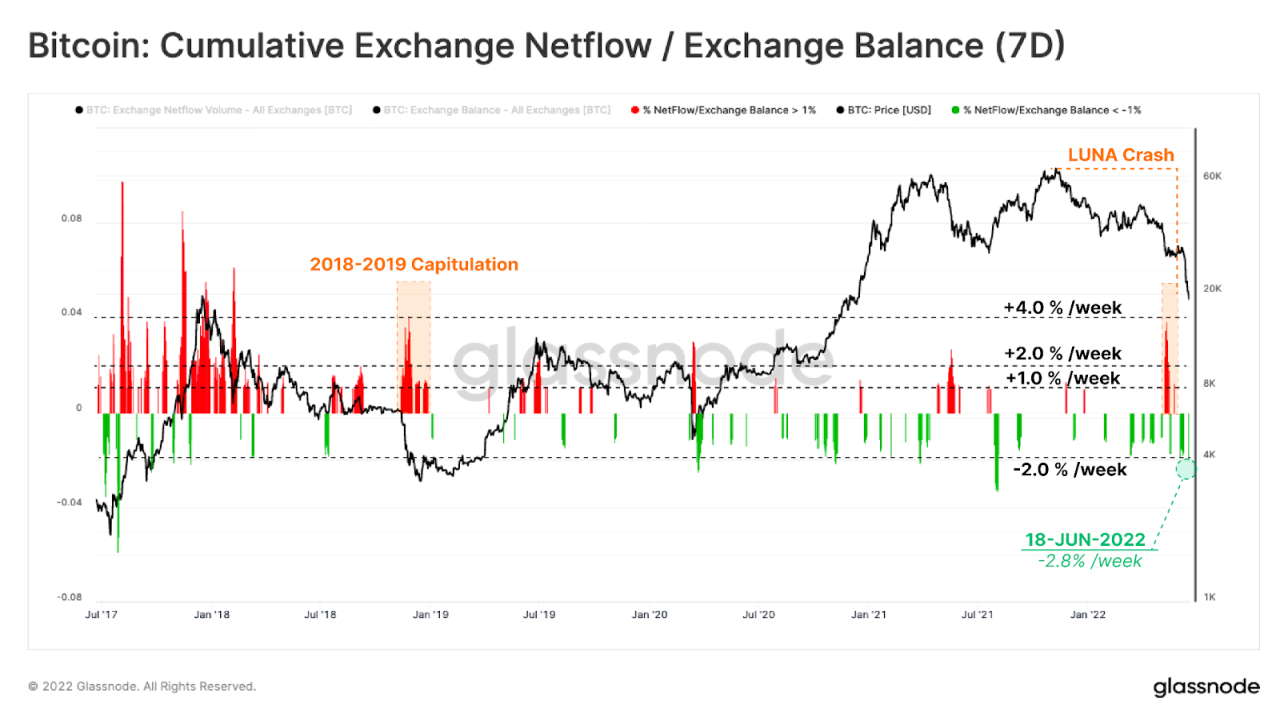

The netflow balance, which is also known as inflows or outflows, will be our final focus. If we observe market inflows into exchanges, it is likely that market participants want to sell their tokens. If we observe market outflows to exchanges we can conclude that market participants want their tokens.

On the right, you can see a strong inflow to the market during May 2022 due to the LUNA crisis. These inflows averaged +4% per semaine (exchange balance). This was similar to the 2018-2019 sell off (>1% of exchange balance inflows).

In spite of the recent sell-off (June), we have noticed a weekly outflow rate of 2.8%. The uniqueness of this sell-off can explain why. Participants may have felt compelled to transfer their tokens into self-custody because of concerns about the creditworthiness and risk perception of large crypto players.

According to the summary, there were back-to–back market sell-offs in May 2022 and June 2022. Despite the fact that these sell-offs were triggered by strong macroeconomic headwinds two black Swan events (namely, the LUNA collapse and insolvency 3AC among other major players) could have contributed to excessive selling. These events may have signaled a bottom at the local level. In the long-term, however, it’s likely that the macro picture will continue to have a strong influence on the markets.

Images CreditsShutterstock. Pixabay. Wiki Commons

{kind=link}